First off, there's a terrific column called:"I Said What?" - a look back at nine regrettable comments by bank chief executive officers.

At #1: John Thain, CEO of Merrill Lynch

"We're very confident that we have the capital base now that we need to go forward in 2008." January 18, 2008.

"...Today I can say that we will not need additional funds. These problems are behind us. We will not return to the market." March 8, 2008

"We have more capital than we need, so we can say to the market that we don't need more injections. We can confirm that we have tackled the problem." March 16, 2008

John Thain learned the hard way that saying the same thing over and over won't necessarily make it come true. The truth is, Merrill was far from finished tapping the markets. Earlier this month, it raised $8 billion by selling stakes in Bloomberg and Financial Data Services. And on Monday it announced plans to sell $8.5 billion of new shares.

See the rest here

Next up, an outstanding column by a trader I have a huge amount of respect for, Todd Harrison. Todd is a very smart guy, well connected in the finance community, and amongst other things, the founder of the financial blog Minyanville.

His column at MarketWatch is very insightful. He writes about the potential consequences of eliminating the practice of shorting stocks, specifically financial stocks, and how eliminating these shorts also eliminates a layer of demand to purchase stocks in a downturn.

TODD HARRISON

Hanky panky

Commentary: Are we trading against Hank Paulson?

By Todd Harrison

Last update: 12:01 a.m. EDT July 30, 2008

NEW YORK (MarketWatch) -- They say the friction between opinions is where true education lies. If that's true, we've officially entered the realm of higher learning.

As both sides of the societal chasm haggle over how the market -- and, by extension, the economy -- is being handled, Treasury Secretary Hank Paulson has found himself in the center of the storm.

Perhaps that's a fitting role for the former chairman of Goldman Sachs a man who deftly sold his equity holdings tax-free when he took the position in 2006. If anyone knows how the game is played, it's Hammering Hank. When pressed on policy, he recently responded, "I'm playing the hand I've been dealt."

Fair enough and truth be told, there isn't a realistic solution other than the elixir of time and price. It just so happens that we've all got chips on this particular table as he draws his next card.

Sucker's bet

We can wag our finger that the writing was on the wall since the subprime simmer of last summer. See MarketWatch column.

We can point to Alan Greenspan, who sowed the seeds of cumulative imbalances during the Asian contagion and tilled them anew after the technology bubble burst. See MarketWatch column.

Wall Street, repackaging risk and masking the disease with years of financial engineering, deserves a dishonorable mention as we dissect the discussion. See MarketWatch column.

Wednesday, July 30, 2008

Wednesday, July 16, 2008

Mortgage Spreads Rising

With greater risk coming from high foreclosure/default rates as we progress through this cycle, spreads between mortgages and treasury securities continue to widen.

The above chart is from Calculated Risk. http://calculatedrisk.blogspot.com/2008/03/mortgage-rates-and-ten-year-treasury.html

Sunday, July 13, 2008

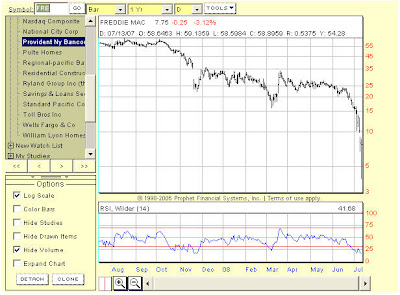

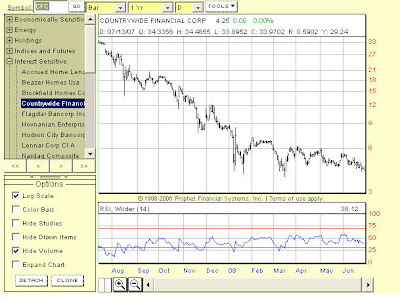

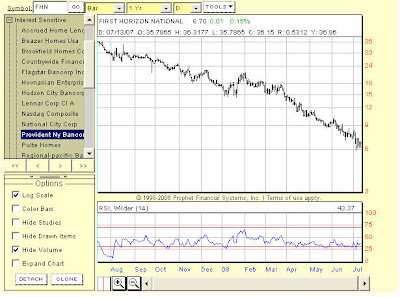

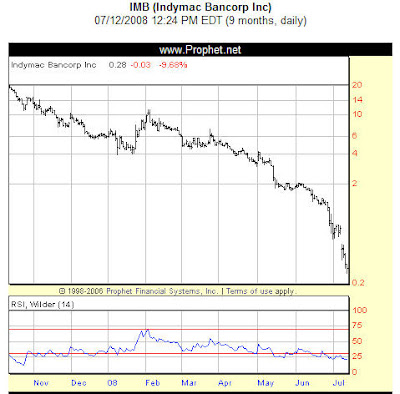

Pictures Worth A Thousand Words

Here are a few stock charts of various mortgage lenders.

Not identical charts, but reasonably similar.

Fannie Mae

Freddie Mac

Countrywide

Washington Mutual

National City

First Horizon

Indymac

Saturday, July 12, 2008

Indymac Bank R.I.P.

From Saturday, June 28 Mortgage Strategery Entry:

"I could see at least a half dozen major wholesale mortgage lenders close their doors in the next six months. I'm not naming names at this point, but I've got several lenders on my major distress list."

Yes, Indymac Bank was on the list.

Honestly, IMB was the most obvious name on the list, but they're one of our lenders, so out of courtesy, I don't want to name specific lender names in public. I simply steer away from them and don't send them any loans unless I absolutely have to, because there's nothing worse than having a loan with a lender that is going out of business. You've got to re-submit with a new lender, if it's a purchase transaction, you lose a great deal of time, and it's frustrating for everyone involved.

Ok, so how do I come up with my distress list. Pretty easy actually. Two steps: 1) Banks that are still in business that used to do a lot of Alt-A and Option Arm business, 2) Look at the stock price, has it nose-dived and is not pulling out of the nose-dive?

"I could see at least a half dozen major wholesale mortgage lenders close their doors in the next six months. I'm not naming names at this point, but I've got several lenders on my major distress list."

Yes, Indymac Bank was on the list.

Honestly, IMB was the most obvious name on the list, but they're one of our lenders, so out of courtesy, I don't want to name specific lender names in public. I simply steer away from them and don't send them any loans unless I absolutely have to, because there's nothing worse than having a loan with a lender that is going out of business. You've got to re-submit with a new lender, if it's a purchase transaction, you lose a great deal of time, and it's frustrating for everyone involved.

Ok, so how do I come up with my distress list. Pretty easy actually. Two steps: 1) Banks that are still in business that used to do a lot of Alt-A and Option Arm business, 2) Look at the stock price, has it nose-dived and is not pulling out of the nose-dive?

Also, Indymac Bank pulled out of the construction lending business back in January.

I knew there was a big problem at IMB because we had an extremely strong construction loan (very strong borrower) with IMB back in December '07, and IMB Construction Underwriting kept coming up with really lame issues regarding the loan: huge cut to LTV because the property was 20.1 acres and not 20 acres, they cut the appraisal value by $40,000 when the appraisal was based on cost basis because comps were too far apart (just as an fyi, in some parts of the country there aren't many comparable sales in the area, especially when the closest neighbor is 10 miles away). When lenders start doing stuff like Indymac was pulling, I take it as a cue that something is wrong with the company because they are giving us reasons not to do the loan with them, basically begging us to pull the loan. Which I did.

I knew there was a big problem at IMB because we had an extremely strong construction loan (very strong borrower) with IMB back in December '07, and IMB Construction Underwriting kept coming up with really lame issues regarding the loan: huge cut to LTV because the property was 20.1 acres and not 20 acres, they cut the appraisal value by $40,000 when the appraisal was based on cost basis because comps were too far apart (just as an fyi, in some parts of the country there aren't many comparable sales in the area, especially when the closest neighbor is 10 miles away). When lenders start doing stuff like Indymac was pulling, I take it as a cue that something is wrong with the company because they are giving us reasons not to do the loan with them, basically begging us to pull the loan. Which I did.

Sure enough, about two weeks later (in January of '08), Indymac announced that they were exiting the construction lending business.

There are other lenders that I'm pretty certain will meet the same fate as IMB.

Saturday, July 12, 2008:

http://www.bizjournals.com/atlanta/stories/2008/07/07/daily91.html

Feds shuts down IndyMac Bank, two ATL centers impacted

Federal regulators closed Pasadena, Calif.-based Indymac Bank late Friday -- the shuttering of the largest bank nationwide since the Savings & Loan Crisis in 1991, and a move that will affect two Atlanta operations centers.

The closure also marks the second-largest closure of a bank since 1934, according to the Federal Deposit Insurance Corp.

In a unique twist, IndyMac Bank's closure is blamed, in part, by the public disclosure of a letter by U.S. Sen. Charles Schumer (D-N.Y.), expressing concern about the bank's ability to operate going forward.

The bank had $32 billion in assets and $19 billion in deposits, according to the Office of Thrift Supervision and FDIC.

At the time of closing, the bank had roughly $1 billion in uninsured deposits.

The FDIC announced the roughly 10,000 customers with uninsured deposits will receive their deposit amounts.

The FDIC also said it expects the fund to pay between $4 and $8 billion out of its deposit insurance fund, which backstops all U.S. bank deposits to a certain dollar level, in part to stave off a deposit run on banks.

At the start of the 2008, the FDIC insurance fund had $52.2 billion in assets.

Indymac Bank is the largest U.S. bank failure since Jan. 6, 1991, when the Bank of New England, with $22 billion in assets, failed.

Regulators are preparing the institution for future sale, and the FDIC was named conservator of the bank's assets, meaning the collapse of the bank happened so quickly FDIC did not have time to arrange a sale of the bank's assets before closing it.

In a statement, the OTS said:

"The immediate cause of the closing was a deposit run that began and continued after the public release of a June 26 letter to the OTS and the FDIC from Senator Charles Schumer of New York. The letter expressed concerns about IndyMac's viability. In the following 11 business days, depositors withdrew more than $1.3 billion from their accounts."

IndyMac Bancorp Inc. and its subsidiary bank, federally chartered thrift IndyMac Bank, operated a large national mortgage business reliant on low documentation mortgage loans, known as Alt-A mortgages.

IndyMac operated two metro Atlanta operations centers, according to its 2007 annual report: A regional mortgage banking center in Norcross, and subsidiary Financial Freedom's Eastern Operations Center in Atlanta.

It is unclear how many employees will be impacted by the closure in metro Atlanta.

The closure comes on the heels of the bank announcing July 7 it was shuttering much of its lending business and cutting 3,400 of its 7,200 employees.

There are other lenders that I'm pretty certain will meet the same fate as IMB.

Saturday, July 12, 2008:

http://www.bizjournals.com/atlanta/stories/2008/07/07/daily91.html

Feds shuts down IndyMac Bank, two ATL centers impacted

Federal regulators closed Pasadena, Calif.-based Indymac Bank late Friday -- the shuttering of the largest bank nationwide since the Savings & Loan Crisis in 1991, and a move that will affect two Atlanta operations centers.

The closure also marks the second-largest closure of a bank since 1934, according to the Federal Deposit Insurance Corp.

In a unique twist, IndyMac Bank's closure is blamed, in part, by the public disclosure of a letter by U.S. Sen. Charles Schumer (D-N.Y.), expressing concern about the bank's ability to operate going forward.

The bank had $32 billion in assets and $19 billion in deposits, according to the Office of Thrift Supervision and FDIC.

At the time of closing, the bank had roughly $1 billion in uninsured deposits.

The FDIC announced the roughly 10,000 customers with uninsured deposits will receive their deposit amounts.

The FDIC also said it expects the fund to pay between $4 and $8 billion out of its deposit insurance fund, which backstops all U.S. bank deposits to a certain dollar level, in part to stave off a deposit run on banks.

At the start of the 2008, the FDIC insurance fund had $52.2 billion in assets.

Indymac Bank is the largest U.S. bank failure since Jan. 6, 1991, when the Bank of New England, with $22 billion in assets, failed.

Regulators are preparing the institution for future sale, and the FDIC was named conservator of the bank's assets, meaning the collapse of the bank happened so quickly FDIC did not have time to arrange a sale of the bank's assets before closing it.

In a statement, the OTS said:

"The immediate cause of the closing was a deposit run that began and continued after the public release of a June 26 letter to the OTS and the FDIC from Senator Charles Schumer of New York. The letter expressed concerns about IndyMac's viability. In the following 11 business days, depositors withdrew more than $1.3 billion from their accounts."

IndyMac Bancorp Inc. and its subsidiary bank, federally chartered thrift IndyMac Bank, operated a large national mortgage business reliant on low documentation mortgage loans, known as Alt-A mortgages.

IndyMac operated two metro Atlanta operations centers, according to its 2007 annual report: A regional mortgage banking center in Norcross, and subsidiary Financial Freedom's Eastern Operations Center in Atlanta.

It is unclear how many employees will be impacted by the closure in metro Atlanta.

The closure comes on the heels of the bank announcing July 7 it was shuttering much of its lending business and cutting 3,400 of its 7,200 employees.

Saturday, July 5, 2008

For Real Estate Agents and Brokers

Distressed Properties Law - HB 2791

Oi, talk about pouring gasoline on a fire. Thank goodness I'm not a realtor. HB 2791 adds a huge layer of legal burdens on realtors and real estate agents when it comes to dealing with individuals with distressed properties.

This is one of the easiest predictions I can make: realtors and real estate agents will simply walk-away from dealing with homeowners with distressed properties. It's not worth the legal liability.

For a distressed homeowner, the bottom line is that in their most dire time of need, there will be very little assistance/counsel coming from Realtors, because the legal risk imposed on Realtors by the State of Washington is extraordinarily onerous. The message for homeowners who are on the brink of losing their homes; don't expect any help from real estate agents. They've got a legal gun being held to their head by the State of Washington if they offer you any help; in many respects, the agents are being expected to be perfect. Perfect in the amount that they are able to sell your home for, perfect in how much they're listing your home for; and to be perfect within the context of 20/20 hindsight with the threat of lawsuit dangling over their head, for no other reason than they are trying to help homeowners desperately in need of assistance.

Here's a link fron the Washington Realtor's website discussing the implications of HB 2791.

http://www.warealtor.org/dpmedia/dvd.asp

Oi, talk about pouring gasoline on a fire. Thank goodness I'm not a realtor. HB 2791 adds a huge layer of legal burdens on realtors and real estate agents when it comes to dealing with individuals with distressed properties.

This is one of the easiest predictions I can make: realtors and real estate agents will simply walk-away from dealing with homeowners with distressed properties. It's not worth the legal liability.

For a distressed homeowner, the bottom line is that in their most dire time of need, there will be very little assistance/counsel coming from Realtors, because the legal risk imposed on Realtors by the State of Washington is extraordinarily onerous. The message for homeowners who are on the brink of losing their homes; don't expect any help from real estate agents. They've got a legal gun being held to their head by the State of Washington if they offer you any help; in many respects, the agents are being expected to be perfect. Perfect in the amount that they are able to sell your home for, perfect in how much they're listing your home for; and to be perfect within the context of 20/20 hindsight with the threat of lawsuit dangling over their head, for no other reason than they are trying to help homeowners desperately in need of assistance.

Here's a link fron the Washington Realtor's website discussing the implications of HB 2791.

http://www.warealtor.org/dpmedia/dvd.asp

Subscribe to:

Posts (Atom)