Interest Rates are declining today: a "perfect storm" for those looking to refinance, with the window of opportunity opening today. As I write this email, the interest rate on the 10 Year Treasury note is at 1.98%. While 30 year fixed mortgage rates don't move in 100% lockstep with 10 Year Treasuries, the correlation is extremely high; think of a tether linking the 30 Year Fixed Mortgage rate and the 10 Year Treasury Note.I am writing this email while watching Jon Corzine testify in front of Congress. It's a very sad day for the former CEO of Goldman Sachs and the recent CEO of MF Global to say under oath that he doesn't know where the money went.But this email is not about Jon Corzine's testimony, per se. It is about a "Perfect Storm" that appears to be unfolding that may, potentially, lead to slightly lower interest rates in the immediate near future.The "Perfect Storm" is 1) the combination of the failure of the EU to come to a meaningful agreement, essentially buying more time because fundamentally the countries are having immense difficulty coming to an agreement to resolve their issues, and 2) a lack of liquidity in the financial futures markets that has resulted from the MF Global fiasco. Up until now, this lack of liquidity, since the October 31, 2011 bankruptcy of MF Global hasn't had a catastrophic impact on the financial markets. But with the potential severity of the EU situation combined with the reduced liquidity in the financial markets from the MF Global fiasco, we may be facing somewhat temporary, but very upsetting "Risk Off" trade, meaning money would be temporarily flowing on a major scale into US Treasuries, perceived to be a safe haven. With interest rates under 2% on the 10 Year Treasury, it seems that process has begun. The question is: will it continue, and if so, how far? History of EU SummitsHat Tip to Barry Ritholtz' The Big Picture Blog link

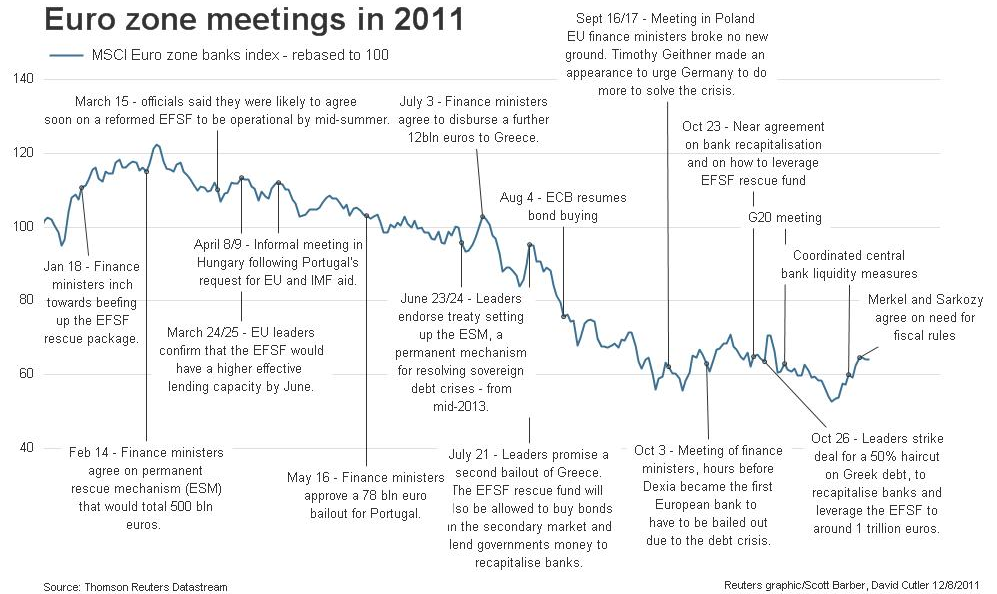

(click on link to see chart)As we can see above, we've had many Euro Zone meetings in 2011 to address the European debt crisis. And the net effect of these meeting has been disappointment, and it appears that today's summit is going to be disappointing as well.Now, as I write this email, we don't know the final announcement from European leaders. That will come out in the wash tomorrow. Maybe there will be a pleasant surprise for the markets to cheer.If we get a "pleasant surprise" from the markets, the short term effect will be a relief rally in "Risk On" assets and a selloff in "Risk Off" assets. To simplify matters, "Risk On" assets are assets like stocks and commodities. "Risk Off" assets are U.S. Treasury Bonds and mortgage backed securities. In short, "Good News" means higher interest rates, "Bad news" means lower interest rates.So if we get "bad news", implying lower interest rates, the big question is "how much lower can interest rates go?". The answer is, historically, not that much lower, but enough to make a difference in your refinance rate. It's critical that if you are looking to refinance right now, that you have someone watch the interest rate market like a hawk, with a finger on the lock trigger.The History Of Interest Rates - A Guaranteed LongshotBelow is the graph, from the Federal Reserve Bank of St. Louis link, of the daily closing yield of the US 10 Year Treasury from January 1, 1962 to December 6, 2011.As I write this email, the U.S. Treasury 10 Year yield is at 1.98%. To put this yield into historical context, I have downloaded all of the days in the above chart, a total of 13,026 days, from January 1, 1962 to December 6, 2011. Out of these 13,026 days, there has been a grand total of 19 days, all of them in 2011, with interest rates below 2%. Most people would look at a 19 out of 13,026 chance as being an incredible long shot, a long shot not even worth considering or thinking about because, well, let's face it a 19 out of 13,026 long probably is not going to happen. But in this case, today, if you are looking to refinance, we have a guaranteed opportunity to lock in a 19 out of 13,026 long shot. It's literally here today.Now putting together the historical opportunity presented above, there is also the practical matter of refinancing. If you do not have a loan application in the system, you need to begin the process. It only takes a few minutes of time on the phone. Once we get an automated approval, we can get the lock process started.

Can interest rates go lower?

I'm going to surprise some folks when I say this, but if the official EU announcement is perceived by the markets as disappointing, then the answer to this question in yes, it is possible that we may see interest rates going slightly lower than where they are at right now. But we also know that interest rates simply don't stay below 2% for very long. Some sort of crisis pushes the rates below 2% for a few days (think of a beach ball pushed below the water and then popping back up quickly) , and then the economic pressures causing the rates to go below 2% ease up, and rates pop back up. Historically, the lowest interest rate on the 10 Year Treasury in the Fed's database, from 1962 to today, was on September 22, 2011 at a rate of 1.72%. Here are all the interest rates below 2%, from 1962 to today.

| Date | Interest Rate |

| | |

| 2011-09-22 | |

| 2011-10-03 | |

| 2011-10-04 | |

| 2011-09-23 | |

| 2011-09-21 | |

| 2011-11-23 | |

| 2011-09-26 | |

| 2011-09-30 | |

| 2011-10-05 | |

| 2011-09-09 | |

| 2011-09-12 | |

| 2011-11-22 | |

| 2011-09-20 | |

| 2011-11-17 | |

| 2011-09-19 | |

| 2011-11-21 | |

| 2011-11-25 | |

| 2011-11-28 | |

| 2011-09-06 | |

| 2011-09-29 |

1.72

1.80

1.81

1.84

1.88

1.89

1.91

1.92

1.92

1.93

1.94

1.94

1.95

1.96

1.97

1.97

1.97

1.97

1.98

1.99

If you are considering refinancing your mortgage, I would say that this rare window of opportunity is now open. "Guaranteed" longshots rarely come along in life, and when they do, one needs to be prepared to take advantage of the opportunity that presents itself.

Note:this is the text version of an email sent to clients. I'm posting this via posterous, which does not allow me to include the graphs. For those that want the original email, I can be contacted at dan.mellis@htlkirkland.com

{kind=link}

No comments:

Post a Comment